Most businesses sign contracts the same way they did thirty years ago: a lawyer drafts it, both parties sign it, and when a dispute arises, someone digs it out and involves another lawyer. It works, but it is slow, expensive, and dependent on intermediaries at every stage.

Blockchain is changing that through self-executing agreements called smart contracts. The global smart contracts market was valued at $2.72 billion in 2024 and is projected to reach $18.18 billion by 2033. More than 80% of the world's largest companies are already working on blockchain solutions. This guide explains what smart contracts are, how they work, and what it means for your business.

What Is a Smart Contract? (The Plain-Language Version)

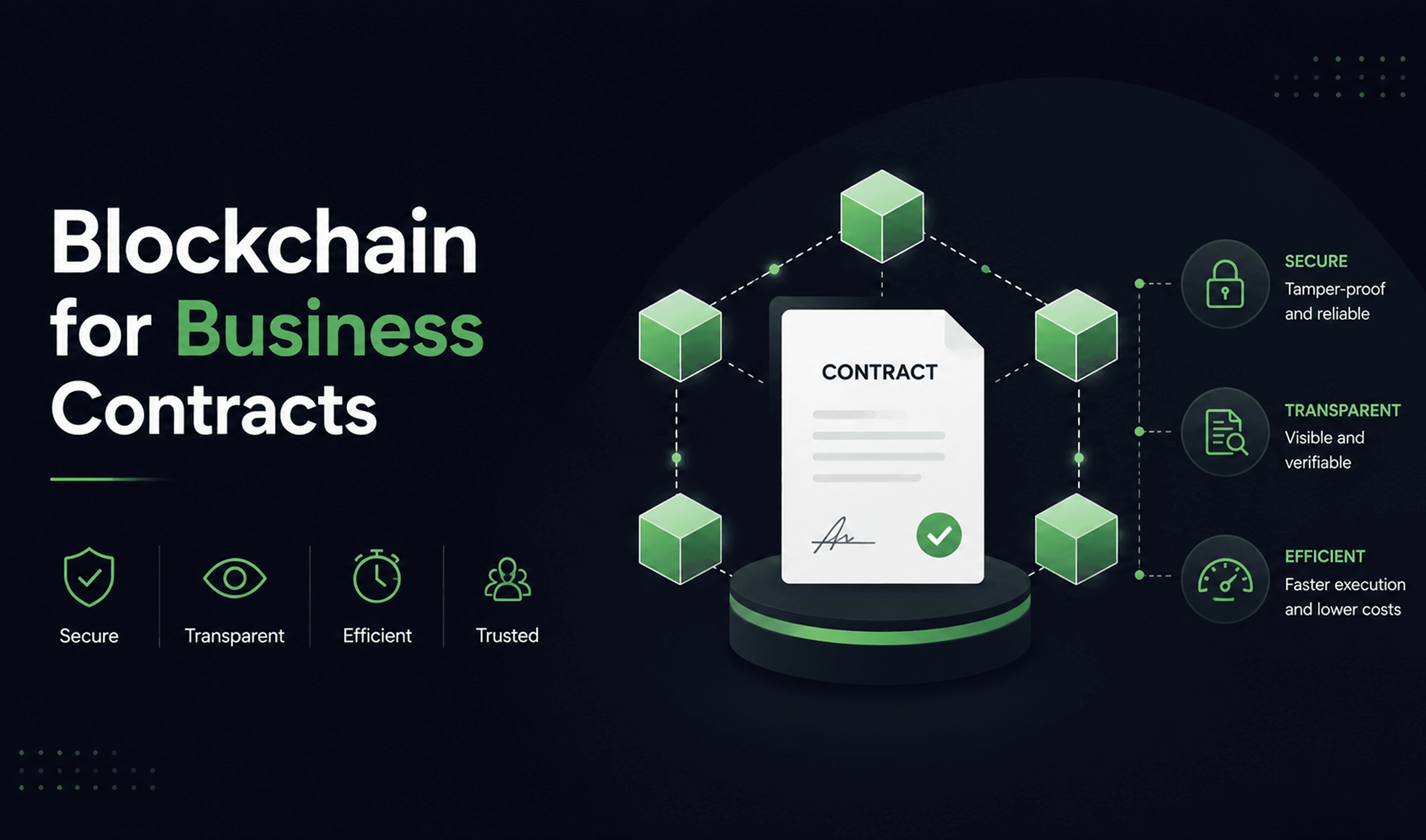

A smart contract is a self-executing agreement written in code and stored on a blockchain. Instead of relying on lawyers, banks, or brokers to enforce its terms, a smart contract enforces itself automatically, executing the agreed actions when predefined conditions are met.

The simplest analogy is a vending machine. You put money in, select your item, and the machine delivers it: no cashier, no human judgment, no possibility of the machine giving you a different product or keeping your money without delivering. The rules are built into the machine. Once you meet the condition (payment), the outcome happens automatically (product delivered).

A smart contract works the same way. If a supplier delivers goods confirmed by a tracking system, payment is automatically released from escrow to the supplier. No invoice needed. No accounts payable team to review and approve. No payment delay. No dispute about whether delivery occurred. The contract handles it all instantly and transparently.

Unlike a regular contract, a smart contract:

- Cannot be altered after it has been deployed

- Executes automatically when conditions are met, without human intervention

- Is visible to all parties in the agreement

- Stores a permanent, tamper-proof record of every transaction on the blockchain

As of mid-2025, over 6.1 million smart contracts are deployed monthly across major blockchain platforms like Ethereum, Solana, and Avalanche.

What Makes Blockchain the Right Foundation for Contracts?

Smart contracts need to run on a system that all parties can trust equally. That is where blockchain comes in.

A blockchain is a distributed ledger: a record of transactions stored simultaneously across thousands of computers rather than in a single location controlled by one party. Because no single party controls the ledger, no single party can alter it unilaterally. Every record is permanent, transparent, and verifiable by anyone with access to the network.

This makes blockchain uniquely suited to contracts for several reasons:

- Immutability. Once a smart contract is deployed on a blockchain, it cannot be changed. The terms you agreed to will be executed. There is no possibility of one party quietly altering the agreement after the fact.

- Transparency. All parties can see exactly what the contract does and when it has been executed. There are no hidden clauses and no ambiguity about whether a condition has been met. The record is there for everyone to verify.

- Decentralisation. No single intermediary, no bank, no escrow service, no legal firm needs to be trusted to hold or execute the agreement. The blockchain network itself is the trusted party, operating according to rules that no individual can override.

- Security. Blockchain records are encrypted and distributed, making them extremely difficult to hack or manipulate. Once a transaction is recorded, it is essentially permanent.

These properties are what transform a piece of code into a trustworthy business agreement and what make smart contracts genuinely disruptive to how commercial relationships are managed.

How Do Smart Contracts Actually Work? (Step by Step)

You do not need to understand the code to understand the process. Here is what happens in practice:

- Agreement. Two or more parties agree on the terms of their arrangement: what each party will do, under what conditions, and what happens if those conditions are or are not met.

- Coding. Those terms are translated into code by a developer. The code defines the conditions and the outcomes: "If the logistics API confirms delivery, release payment. If delivery is not confirmed within 30 days, return funds to the buyer."

- Deployment. The coded contract is deployed onto a blockchain network. Both parties can review it. Once deployed, it cannot be changed.

- Execution. When the conditions are met, perhaps a logistics system confirms delivery or a payment clears, the smart contract executes the agreed outcome automatically. No human needs to approve or trigger it.

- Record. Every execution is permanently recorded on the blockchain. Both parties have an immutable audit trail showing exactly what happened and when.

The practical result is that agreements between businesses can now be executed in minutes rather than days, without requiring either party to trust the other, because they both trust the code.

Where Are Businesses Already Using Smart Contracts?

This is no longer theoretical. Smart contracts are in active commercial use across a wide range of industries. Here are the most significant applications for business contracts specifically.

Supply Chain and Procurement

Supply chains involve multiple parties: manufacturers, logistics providers, customs authorities, distributors, retailers, and enormous volumes of contracts, invoices, and payments. Traditional contract management across these networks is slow, error-prone, and ripe for fraud. Smart contracts automate the handoffs. Payment is released when a shipment is confirmed. Customs documentation is triggered when goods cross a border. Quality checks unlock the next stage of the process. According to McKinsey, blockchain-based trade processing has compressed letter of credit transactions that previously took up to ten days down to under four hours. Walmart and Amazon are among the major corporations that have integrated blockchain-based tracking and contract automation into their supply chain operations.

Freelancer and Vendor Payments

For businesses that work with freelancers, agencies, or project-based vendors, payment disputes are a recurring headache. A smart contract eliminates them. Payment is held in escrow and released automatically when agreed milestones are confirmed, without either party needing to chase, dispute, or negotiate. A retailer could onboard new suppliers in minutes instead of weeks through automated agreement templates. Agencies, vendors, and freelancers receive payment without follow-ups or disputes, improving cash flow and reducing operational friction for both sides.

Real Estate Transactions

Property transactions typically involve estate agents, solicitors, mortgage providers, land registries, and weeks or months of paperwork. Smart contracts automate the title transfer, confirmation of payment, and update of ownership records, compressing a process that takes months into one that can happen in hours. Platforms like Propy and Ubitquity are already facilitating real estate transactions on blockchain, with property titles transferred automatically once payment is confirmed.

Legal Agreements and NDAs

Business legal agreements, non-disclosure agreements, service contracts, and licensing agreements can be stored on blockchain as tamper-proof records accessible to all authorised parties. More significantly, conditions within those agreements can be made self-enforcing. Platforms like the Accord Project allow contract clauses like "pay in 30 days" to be written as executable code, so payment triggers automatically rather than requiring manual processing and potential dispute. A small business can save thousands annually by avoiding lawyer fees for drafting and enforcing contracts that can be standardised and automated.

Insurance Claims

Insurance is an industry notorious for slow, complex, and often disputed claims processes. Smart contracts are changing this in specific, high-volume use cases. Travel insurance companies are already using smart contracts that automatically pay compensation for flight delays when the delay data is confirmed by a connected flight tracking system: no claim form, no adjuster, no waiting. According to a PwC report on blockchain in reinsurance, implementing blockchain in insurance could open up $5 to 10 billion in cost savings through faster, more efficient claims settlement and compliance processes.

Financial Services and Cross-Border Payments

In November 2024, Mastercard's Multi-Token Network joined with JP Morgan's Kinexys Digital Payments to facilitate cross-border B2B payments through blockchain, enabling near-instant value exchange across time zones, a process that previously took days and involved multiple correspondent banking relationships. Research cited by the World Economic Forum estimates that smart contracts and automated processes in financial infrastructure could drive $15 to 20 billion in annual global cost savings for banks and financial institutions.

The Business Benefits of Smart Contracts

The appeal of smart contracts comes down to a set of consistent, measurable advantages over traditional contract management.

Speed

Traditional contract execution involves review, approval, signature, processing, and payment: each step is dependent on human action, and each step introduces delay. Smart contracts execute instantly when conditions are met. A payment that would take 30 days under standard invoice terms can be processed in seconds.

Cost reduction

Every intermediary in a contract process has a cost. Lawyers. Escrow services. Brokers. Banks. Notaries. Smart contracts remove most of these from the equation. The contract enforces itself. For high-volume, standardised agreements such as supplier payments, royalty distributions, subscription billing, and milestone releases, this cost reduction compounds significantly over time.

Elimination of human error

Manual contract processing introduces errors: invoices entered incorrectly, payments sent to the wrong account, and conditions misread or misapplied. Smart contracts execute exactly as coded, every time, without the variability that human processing introduces.

Transparency and accountability

All parties can see the same version of the contract and the same execution record. There are no hidden terms, no disputed interpretations, no version conflicts. The blockchain record is the definitive, shared source of truth for every party to the agreement.

Tamper-proof records

Once a smart contract transaction is recorded on the blockchain, it cannot be altered or deleted. This creates an audit trail of extraordinary reliability, far more robust than a shared document in a cloud drive or a signed PDF that could be replaced or disputed.

Reduced dispute risk

Disputes arise when there is ambiguity about what was agreed, whether a condition was met, or whether an action was taken. Smart contracts eliminate most of that ambiguity. The conditions are explicit in the code. The execution is automatic and recorded. There is far less room for the good-faith misunderstandings and bad-faith manipulations that drive traditional contract disputes.

The Honest Limitations: What Smart Contracts Cannot Do

A balanced guide requires acknowledging what smart contracts are not yet good at. There are genuine limitations that businesses need to understand before committing to blockchain-based contract management.

Code bugs are permanent and costly

Because smart contracts are immutable once deployed, a bug in the code cannot simply be patched the way you would fix software. Smart contract vulnerabilities have been responsible for significant financial losses across the blockchain industry, making rigorous independent code auditing before deployment essential. That auditing has a real cost and should be treated as non-negotiable.

Legal recognition is still evolving

Smart contracts do not yet have consistent legal recognition across all jurisdictions. Many countries have enacted laws that treat certain smart contract outputs as legally binding, but the legal landscape is still developing and uneven. For contracts where legal enforceability in a specific jurisdiction matters, you need specialist legal advice on how smart contracts interact with the applicable law.

They cannot handle ambiguity

Traditional contracts contain clauses like "reasonable efforts" or "material breach": terms that require human judgment to interpret in context. Smart contracts are binary: a condition is either met or it is not. This makes them excellent for objective, measurable conditions (payment received, goods delivered, deadline passed) and less suitable for complex agreements involving subjective judgment.

They need reliable data inputs

A smart contract is only as reliable as the data it acts on. If the logistics API confirms delivery incorrectly, the payment is released incorrectly. The quality of "oracles" (the external data feeds that smart contracts rely on) is a known challenge in the industry and a critical consideration for any implementation.

Technical expertise is required

Developing, auditing, and deploying smart contracts requires specialist blockchain development skills. This is not a tool a non-technical business owner can build themselves today, though low-code and no-code smart contract platforms are beginning to make this more accessible.

Should Your Business Be Paying Attention to This?

Blockchain for business contracts is not a technology for every business right now. But it is one that more businesses will encounter in the coming years, either as something they adopt or something their partners and customers adopt.

You should be actively exploring smart contracts if:

- Your business processes a high volume of standardised contracts with the same or similar terms (supplier payments, contractor milestones, subscription agreements, royalty payments)

- You operate in industries where transparency and audit trails are critical (finance, healthcare, legal, logistics)

- You regularly work across international borders, where payment delays and currency conversion are friction points

- You have recurring disputes over whether contract conditions have been met

- Your industry peers or major customers are already exploring or adopting blockchain solutions

You may be better served by traditional contract management tools if:

- Your contracts are primarily bespoke, complex, and require significant human negotiation and interpretation

- Your agreement volumes are low, and the cost of smart contract development would not be justified by savings

- You operate in a jurisdiction where the legal status of smart contracts remains unclear

- You do not have access to the technical expertise required to develop and audit smart contracts safely

Getting Started: A Practical Path for Business Leaders

If you have decided that smart contracts are worth exploring for your business, here is a sensible sequence of steps.

- Start with education, not implementation. Before engaging any developer or platform, invest time in understanding the specific use cases where smart contracts would solve a genuine problem for your business. The technology should follow the business case, not the other way around.

- Identify your highest-friction contract process. Where does contract execution cause the most delays, disputes, or administrative costs in your business? That is the candidate for a first smart contract implementation. High-volume, standardised payment agreements are almost always the best starting point.

- Consult a specialist. You need both technical and legal expertise: a blockchain developer to build and audit the contract, and a lawyer familiar with the legal landscape in your jurisdiction to advise on enforceability and compliance.

- Start small and pilot. Do not attempt to move your entire contract management to blockchain at once. Run a pilot with a single supplier or a single contract type. Measure the results. Build understanding and capability before scaling.

- Consider existing platforms. You do not necessarily need to build from scratch. Platforms like the Accord Project, Chainlink, and enterprise blockchain solutions from IBM, Oracle, and SAP offer pre-built frameworks that reduce development cost and time.

Ready to take the next step? Visit our Blockchain Development services page to see how we help businesses design and implement smart contract solutions.

Frequently Asked Questions (FAQ)

1. What is a smart contract in simple terms?

A self-executing agreement written in code on a blockchain. When conditions are met (for example, payment confirmed, goods delivered), it executes automatically with no intermediary needed.

2. How is a smart contract different from a regular contract?

A regular contract requires humans to interpret and enforce it. A smart contract enforces itself automatically when predefined conditions are met. It is binary, instant, and tamper-proof.

3. Is blockchain relevant to small businesses?

Not as a full implementation for most SMBs today, but smart contract logic is already embedded in many payment, supply chain, and freelancer platforms they use. Worth understanding now as adoption accelerates across industries.

4. Are smart contracts legally binding?

In many jurisdictions, including the UK, several US states, and others, they are recognised. But the legal landscape is still evolving, so specialist legal advice in your jurisdiction is essential before relying on them.

5. Can smart contracts replace lawyers?

No. They are excellent at automating clear, objective conditions, but complex agreements requiring human judgment, negotiation, or dispute resolution still need legal expertise.

6. What industries are using smart contracts the most?

Financial services, supply chain and logistics, insurance, real estate, and healthcare are all sectors with high transaction volumes, multiple parties, and a strong need for audit trails.

7. What is the biggest risk of smart contracts?

Code bugs. Because smart contracts are immutable once deployed, errors cannot be patched after the fact. Independent auditing before deployment is non-negotiable.

8. How much does it cost to implement a smart contract?

Simple contracts can cost a few thousand dollars to develop. Complex enterprise implementations with auditing and integrations can run to tens or hundreds of thousands. The business case should drive the investment decision.

Final Thoughts

Blockchain is changing the way businesses handle contracts in practical, measurable ways today, not theoretical and distant ones. The self-executing, tamper-proof nature of smart contracts removes friction, cost, and risk from agreements that traditionally required layers of human intermediaries to function.

This does not mean every business needs a blockchain strategy today. But every business leader benefits from understanding what smart contracts are, where they are already being used, and what problems they solve, because the businesses that do understand this will make better decisions when opportunities or pressures to adopt arise.

The shift from paper to e-signature changed how contracts were signed. Smart contracts represent the next shift: from agreements that humans must enforce to agreements that enforce themselves. That shift is already underway.